119

Financial Information and Risk

Management

İş Bankası

Annual Report 2013

TÜRKİYE İŞ BANKASI A.Ş.

Notes to the Unconsolidated Financial Statements

for the Year Ended 31 December 2013

The acquisition costs of tangible assets other than the land and construction in progress are amortized by the straight-line method,

according to their estimated useful lives. The estimated useful life, residual amount and the method of amortization are reviewed

every year for the possible effects of the changes that occur in the estimates and if there is any change in the estimates, they are

recognized prospectively.

Assets held under finance lease are depreciated over the expected useful life or lease term, whichever is the shorter for the

specified period.

Leasehold improvements are amortized in equal amounts considering their useful life. However, in any case the useful life cannot

exceed leasing term. When the lease period is not certain, or longer than 5 years, the amortization period is recognized as 5 years.

The difference between the sales proceeds arising from the disposal of tangible assets or the inactivation of a tangible asset and

the book value of the tangible assets are recognized in the income statement.

Regular maintenance and repair costs incurred for tangible assets are recorded as expense.

There are no restrictions such as pledges, mortgages on tangible assets.

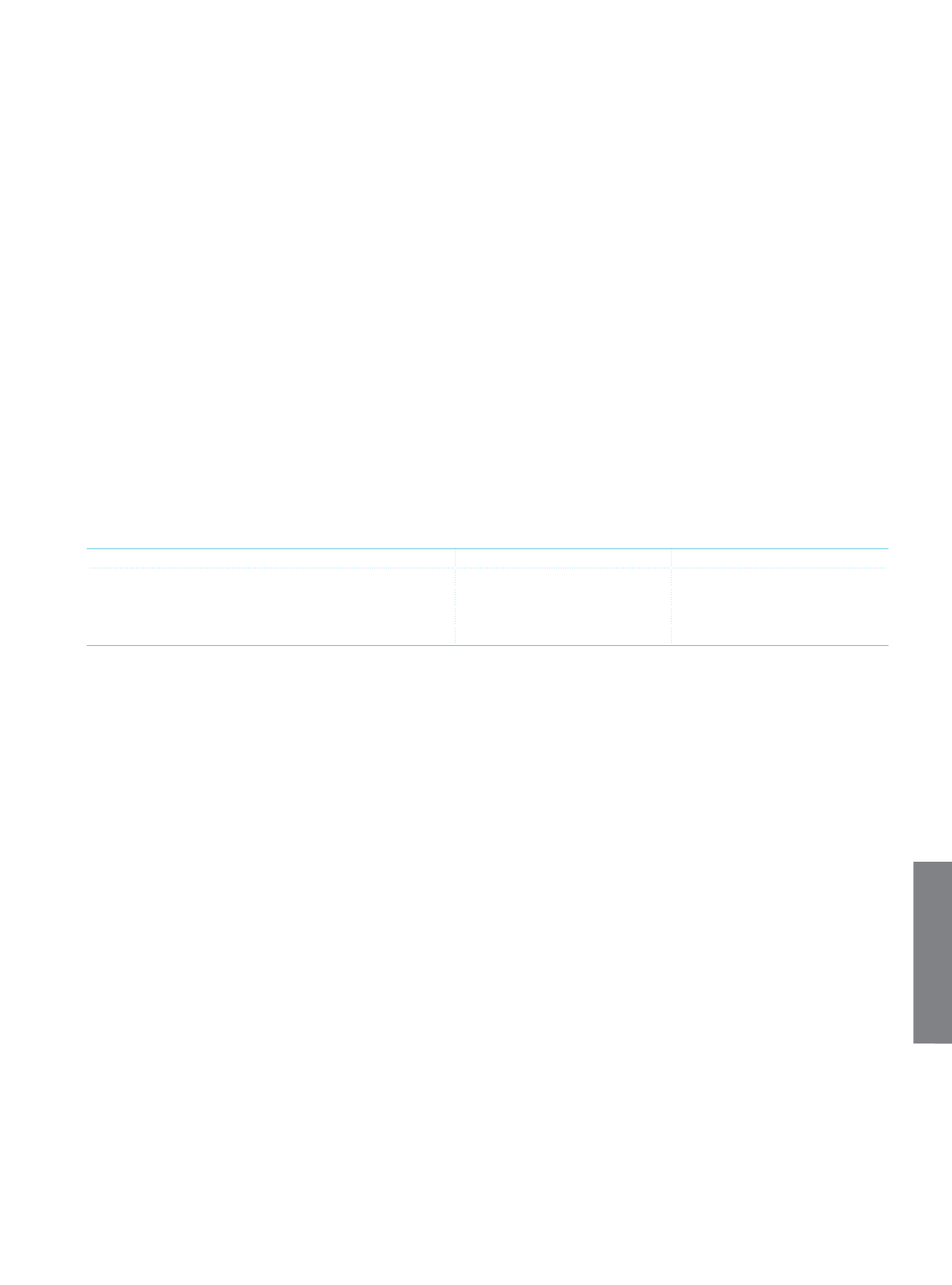

The depreciation rates used in amortization of tangible assets and their estimated useful lives are as follows:

Estimated Economic Life (Year)

Depreciation Rate

Buildings

4-50

2%-25%

Safe Boxes

2-50

2%-50%

Other Movables

2-25

4%-50%

Leased Assets

4-5

20%-25%

XIV. Leasing Transactions

Assets acquired under financial leases are carried at the lower of their fair values or amortized value of the lease payments. Leasing

payables are recognized as liabilities in the balance sheet while the interest payable portion of the payables is recognized as a

deferred amount of interest. Finance lease payments are separated as financial expense and principal amount payment, which

provides a decrease in finance lease liability, thus helps a fixed rate interest on the remaining principal amount of the debt to be

calculated. Within the context of the Bank’s general borrowing policy, financial expenses are recognized in the income statement.

Assets held under financial leases are recognized under the property, plant and equipment (movable properties) account and are

depreciated by using the straight line method.

The Bank does not participate in the financial leasing transactions as a “lessor”.

Operational lease transactions are recognized in line with the related agreement on an accrual basis.

XV. Provisions and Contingent Liabilities

As of the end of the reporting period, A past event is deemed to give rise to a present obligation if, taking account of all available

evidence, it is more likely than not that a present obligation exists, the entity recognizes a provision in the financial statements. As of

the end of the reporting period where it is more likely that no present obligation exists at the end of the reporting period, the entity

discloses a contingent liability, unless the possibility of an outflow of resources embodying economic benefits is remote.

In the financial statements, a provision is made for an existing commitment resulted from past events if it is probable that the

commitment will be settled and a reliable estimate can be made of the amount of the obligation.

Provisions are calculated based on the best estimates of management on the expenses to incur as of the balance sheet date to fulfill

the liability by considering the risks and uncertainties related to the liability.

In case the provision is measured by using the estimated cash flows required to fulfill the existing liability, the book value of the

related liability is equal to the present value of the related cash flows.

If the amount is not reliably estimated and there is no probability of cash outflow from the Bank to settle the liability, the related

liability is considered as “contingent” and disclosed in the notes to the financial statements.