239

Financial Information and Risk

Management

İş Bankası

Annual Report 2013

TÜRKİYE İŞ BANKASI A.Ş.

Notes to the Consolidated Financial Statements

for the Year Ended 31 December 2013

2.

Information on counterparty credit risk:

A counterparty credit risk, which is accounts for trading derivatives and repo transactions tracked on both sides, such as the credit

risk the liability arising from transactions, is determined by the methodology which is used according to the Appendix-2 of the

“Regulation on Measurement and Assessment of Capital Adequacy Ratios of Banks” which is published on the Official Gazette

no.28337 dated 28 June 2012 and became effective starting from 1 June 2007. Counterparty credit risk valuation method based on

the calculation of the fair value of the derivative transactions is implemented. The calculation of the amount of risk on derivative

transactions, the potential amount of credit risk is positively correlated with the sum of the costs of renewal. The calculation of the

amount of the potential credit risk of the contract amount is multiplied by the rates given in the regulation. Derivative instruments

valuation based on replacement costs and the fair value of the related contracts are obtained.

The Bank is exposed to counterparty credit risk is managed within the framework of general principles and guarantees the credit

limit allocation. Exposure to credit risk of derivative transactions with banks due to the majority of reciprocal agreements signed

with related parties are subject to the daily exchange of collateral, counterparty credit risk exposure is reduced in this way. On the

other hand, the calculation of capital adequacy under the legislation of counterparty credit risk, the risk-reducing effect of such

agreements is not considered.

Within the scope of trading accounts with credit derivatives acquired or disposed of by the Bank does not have any protection.

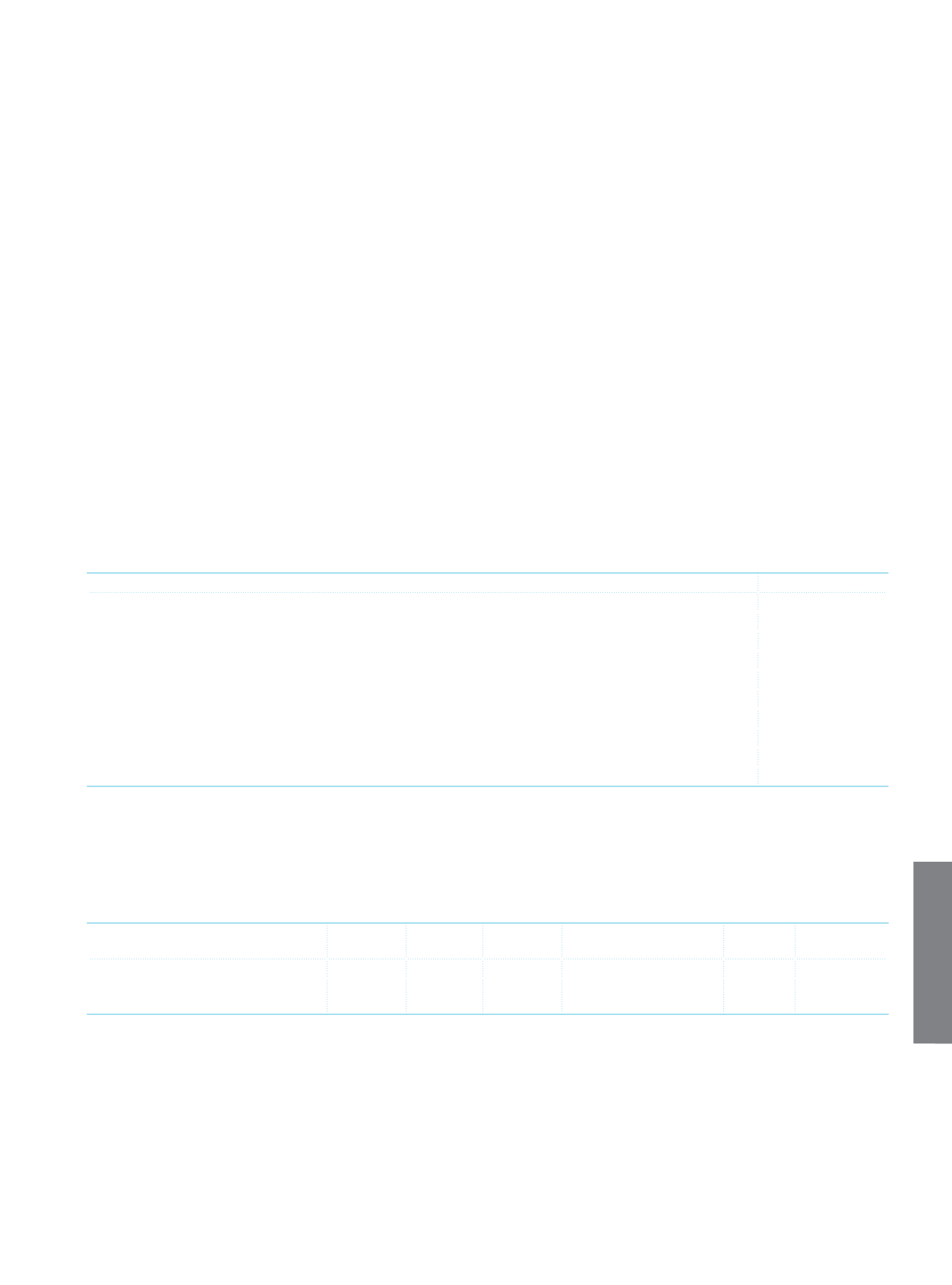

Quantitative information on counterparty risk:

Amount

Interest-Rate Contracts

55,543

Foreign-Exchange-Rate Contracts

459,837

Commodity Contracts

6,988

Equity-Shares Related Contracts

348

Other

Gross Positive Fair Values

1,031,506

Netting Benefits

Net Current Exposure Amount

Collaterals Received

Net Derivative Position

1,554,222

IV. Explanations on Consolidated Operational Risk

The operational risk capital requirement is calculated according to Regulation on Measurement and Assessment of Capital Adequacy

Ratios of Banks’ article number 24, is measured using the Basic Indicator Approach once a year in parallel with domestic regulations.

As of 31.12.2013 the consolidated operational risk amount is TL 13,629,748, information about the calculation is given below.

The information contained in the following table when using the basic indicator method:

2PP

Amount

1PP

Amount CP Amount

Total/Positive Years of

Gross Income Amount Rate (%)

Total

Gross Income

6,316,693 6,967,199 8,523,704

3

15 1,090,380

Value at operational risk

(Total*12.5)

13,629,748